By indi Mortgage

•

July 29, 2026

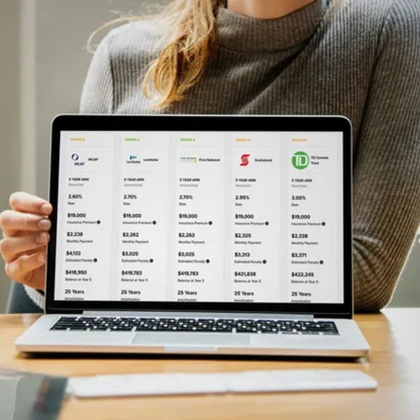

For most Canadians, the down payment is the biggest hurdle to homeownership. A down payment is the initial amount you contribute toward your property purchase, while the lender covers the rest through a mortgage. By law, Canadian lenders can only finance up to 95% of a property’s value, which means you’ll need at least 5% down to qualify. If you’re putting down less than 20%, your mortgage must be insured through one of Canada’s three default insurance providers— CMHC, Sagen (formerly Genworth), or Canada Guaranty . This insurance comes at a cost, but it can be rolled into your mortgage amount. The less you put down, the higher the premium. Since saving a down payment can feel overwhelming, it helps to know the different sources you can draw from. Here are the most common options available to Canadian homebuyers: 1. Savings & Personal Resources The most straightforward source is your own savings. Lenders will ask to see a 90-day history of the funds in your account. Any large deposits outside of regular payroll must be explained with documentation—such as the sale of a vehicle or a transfer from an investment account. This requirement isn’t just red tape; it’s part of Canada’s anti-money laundering rules. 2. Proceeds from the Sale of a Property If you’ve recently sold another home, you can use the proceeds as a down payment on your new purchase. Proof of the sale—such as the final statement of adjustments from your lawyer—will be required. 3. RRSP Home Buyers’ Plan (HBP) First-time buyers can withdraw up to $35,000 each (or $70,000 as a couple) from their RRSPs to put toward a down payment under the federal Home Buyers’ Plan . The funds are withdrawn tax-free, but they must be repaid over a 15-year period. This is a popular option for buyers who have been steadily contributing to their retirement savings. 4. Gifted Down Payment With today’s housing prices, many buyers turn to family for help. A parent or immediate family member can provide a gift that makes up part—or even all—of the required down payment. The lender will require a signed gift letter confirming that the money is a true gift (with no repayment expected) and proof that the funds have been deposited into your account. 5. Borrowed Down Payment In some cases, you may be able to borrow your down payment. This option is usually available only if you have strong credit and sufficient income. The payments on the borrowed funds are factored into your debt service ratios, so affordability is key. Lenders typically use 3% of the outstanding balance when calculating the additional payment. The Bottom Line A down payment doesn’t have to come from just one source—it can be a combination of savings, gifted funds, RRSPs, or other resources. What matters most is being able to show where the money came from and that it meets lender requirements. If you’d like to explore your options or learn how much you might qualify for, it’s never too early to start the conversation. Connect with us today—we’d be happy to help you create a plan and take the first steps toward homeownership.